A 5% Deposit Isn't the Problem. The Mortgage Is.

Government schemes promise to help first-home buyers enter the market. But for many young Australians, the real barrier comes after the deposit is paid.

Arthur Dimitriou lives in a self-contained apartment above his parents' house in Melbourne.

Like many young Australians, he has spent years watching house prices climb further out of reach while trying to save for a home of his own. When the Federal Government expanded its five per cent deposit scheme for first-home buyers, it seemed like the kind of support that could finally make home ownership possible.

But after looking into the scheme, Dimitriou came to a different conclusion.

"The mortgage repayments were still way too expensive for me," he says.

The Federal Government's five per cent deposit scheme allows eligible first-home buyers to purchase a property with a deposit as low as five per cent, while avoiding the additional cost of lenders' mortgage insurance.

The policy is designed to reduce one of the biggest barriers facing aspiring homeowners: saving a large deposit.

Prime Minister Anthony Albanese has described the initiative as a way to help more Australians enter the property market sooner, particularly as housing affordability continues to dominate national political debate.

For buyers like Dimitriou, however, the deposit is only one part of the equation.

While a lower deposit may help people secure a loan, rising property prices and higher interest rates mean the ongoing cost of mortgage repayments can still place home ownership beyond reach.

"I could see how the scheme would help some people," Dimitriou says.

"But when I looked at what I'd actually have to repay every month, it just wasn't realistic."

His experience reflects a broader challenge facing many first-home buyers across Australia.

Property expert Patrick Archer says low deposit schemes can be effective in helping people enter the market, but they do little to address the structural issues driving housing affordability.

"The lowering deposit really does help people," Archer says.

"But all that does is stimulate demand."

Archer argues that Australia's affordability crisis has been building for decades and is driven by a combination of factors, including taxation, regulation, labour shortages and rising construction costs.

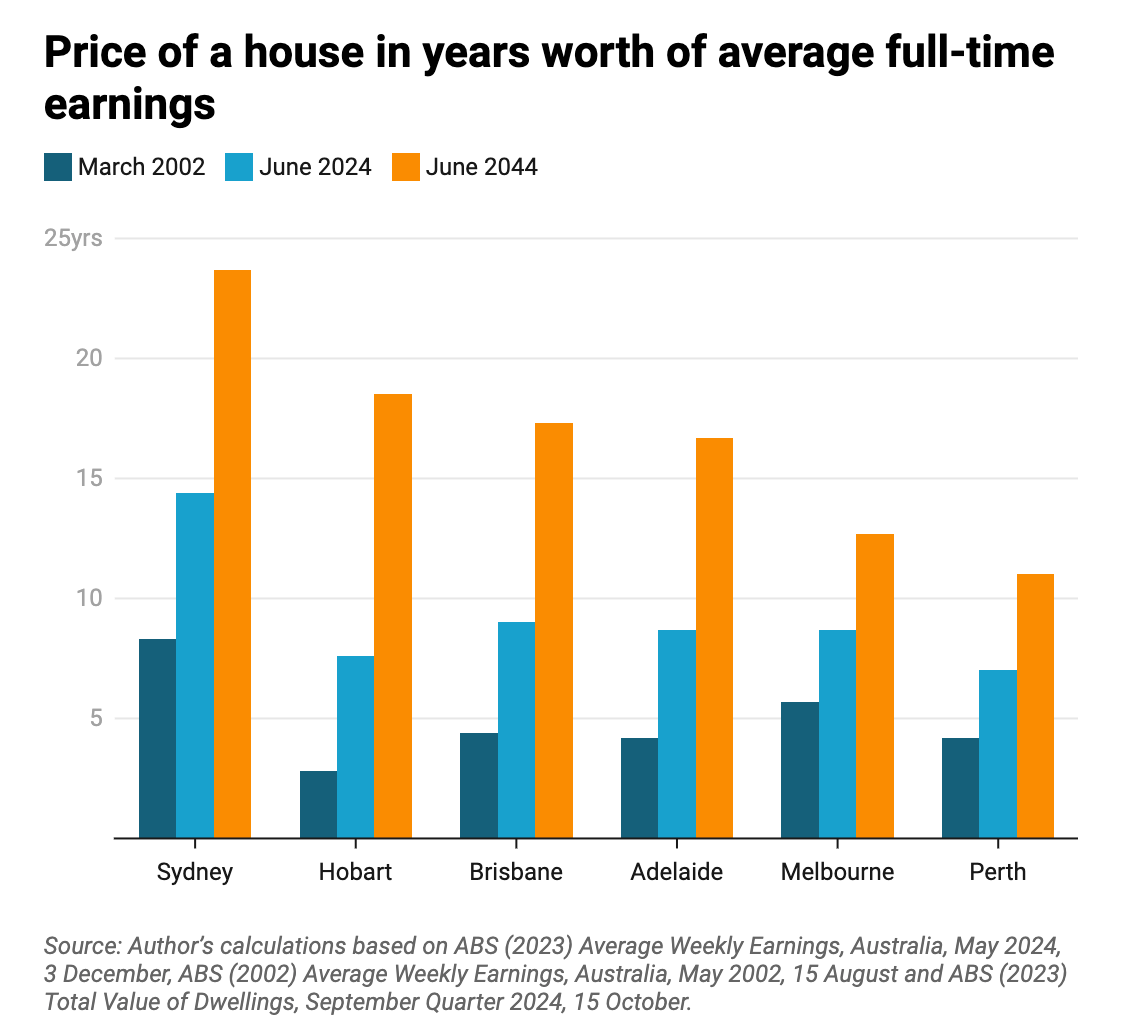

Recent figures from the ANZ/CoreLogic Housing Affordability Report show it now takes the average Australian household around 10.6 years to save a 20 per cent deposit for a median-priced home. That's longer than the historical average and reflects the growing gap between incomes and property prices.

Even after buyers have saved enough to enter the market, ongoing costs remain a significant hurdle. The report found that mortgage repayments on a median-priced dwelling consume more than half of a household's gross annual income, placing many Australians under financial pressure.

House prices have continued to rise faster than wages. Australia's median dwelling value surpassed $800,000 in 2024, while income growth has struggled to keep pace. For buyers like Dimitriou, this means that although government schemes can reduce the upfront cost of purchasing a home, the long-term financial commitment remains daunting.

According to the Housing Industry Association, government taxes and charges make up a significant proportion of the final cost of new homes, adding thousands of dollars to the price buyers ultimately pay.

At the same time, Australia's construction industry continues to face workforce shortages, supply chain pressures and increasing material costs.

These factors have made it more expensive to build new homes, limiting supply and placing further pressure on prices.

"You need both sides," Archer says.

"You need the supply side — how do we increase supply and reduce the cost of supply — as well as helping people get on the ladder."

The distinction is important.

Policies such as the five per cent deposit scheme focus primarily on helping buyers access finance. Experts argue that unless governments also address housing supply and construction costs, affordability challenges are likely to persist.

Recent years have seen Australians face rising interest rates and cost-of-living pressures, further reducing borrowing power.

As a result, many buyers are purchasing smaller homes or delaying their plans altogether.

For Dimitriou, the dream of homeownership remains alive, but it is not something he sees happening in the immediate future.

Instead, he continues to live above his parents' house while monitoring the market and weighing up his options.

His story highlights a reality facing many Australians today.

Government schemes may make it easier to save for a deposit, but affordability does not end once the keys are handed over.

For a growing number of young Australians, the challenge is no longer finding the money to enter the housing market.

It is finding the money to stay in it.